You may be sitting at your kitchen table right now, looking at a missing tooth in the mirror, checking your phone for “dental implants near me,” and worrying that the solution you want won't fit your budget. That mix of frustration and hesitation is common. A gap in your smile can affect how you eat, how you speak, and how comfortable you feel around other people. The price of fixing it can feel just as stressful as the dental problem itself.

Patients in Chattanooga and Cleveland often tell us the same thing. They want something stable and long-lasting, but they don't want to guess their way through financing. Clear information helps. When you understand the total cost, the monthly payment options, and the approval process, treatment starts to feel possible instead of overwhelming.

Affordable Dental Implants in Chattanooga & Cleveland TN

A patient loses a back tooth, waits a few months, and starts chewing on one side. Then photos come up, and that missing front tooth or visible gap suddenly feels bigger than it did at first. By the time they search for a dentist in Chattanooga, TN or dentist near me, they're often carrying two worries at once. They want their smile back, and they're bracing for a number they may not be ready to hear.

That's why implant payment plans matter so much. They turn one large treatment fee into smaller decisions. Instead of asking, “Can I pay for all of this today?” the better question becomes, “What kind of monthly plan can I manage comfortably while moving forward with treatment?”

For many adults in Cleveland and Chattanooga, implants aren't just about appearance. They're part of restorative dentistry that supports daily function. Replacing a missing tooth can help with chewing, speaking, and keeping your bite balanced. In some cases, treatment may also connect with other services such as tooth extraction, full-arch replacement, or cosmetic updates that improve the look of the final result.

Many patients don't need a cheaper treatment. They need a clearer path to paying for the right treatment.

People also get confused because “flexible financing” can mean very different things from one office to another. One plan may be short-term and interest-free. Another may stretch payments longer through an outside lender. Another may ask for a larger deposit up front. Knowing those differences helps you compare options with confidence instead of focusing only on the lowest monthly number.

If you're looking for a dentist in Cleveland, TN, cosmetic dentist near me, or emergency dentist after a broken tooth or sudden loss, the goal is the same. You need answers that feel practical, honest, and easy to use.

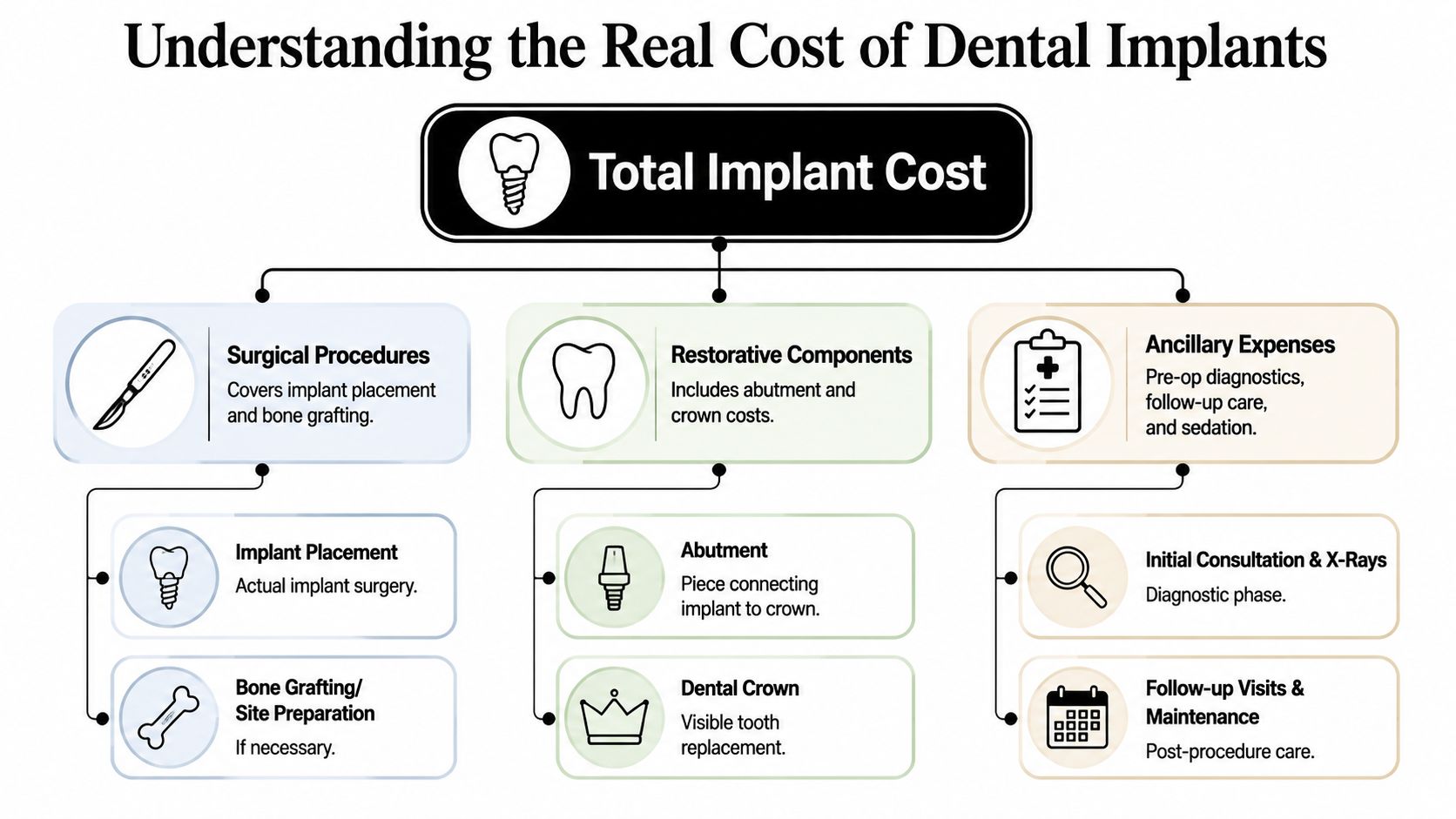

Understanding the Real Cost of Dental Implants

The total fee for an implant can sound high until you see what's included. A dental implant isn't one single item. It's a sequence of clinical steps and custom parts that work together to replace a missing tooth from root to crown.

The average cost for a single dental implant in the United States ranges from $3,000 to $6,000, a price point that typically includes the implant post, abutment, and the dental crown, though costs can vary significantly based on geographic location, case complexity, and bone grafting needs according to this dental implant cost overview.

What you're paying for

The fee usually covers several distinct pieces of treatment:

- Implant post. This is the part placed in the jawbone. It acts like an artificial tooth root.

- Abutment. This small connector joins the implant post to the visible tooth.

- Custom crown. This is the part you see above the gumline. It's designed to match your smile.

- Surgical placement. This includes the clinical work of positioning the implant correctly.

- Preparatory care. Some patients need a tooth extraction, bone grafting, or site preparation before the implant can be placed.

Why costs vary from person to person

Two patients can both need “one implant” and still have different treatment fees. One may have healthy bone and a straightforward placement. Another may need extra healing time, imaging, or grafting before the implant is ready.

That's why online price shopping can feel confusing. A low advertised number may not reflect the full treatment process. It may leave out parts that are necessary for a durable result.

Practical rule: Ask whether the quoted fee includes the implant post, abutment, crown, diagnostics, and follow-up visits. If it doesn't, the “cheaper” option may not actually cost less.

Why many patients see implants as a long-term investment

Bridges and removable options can still be appropriate in some cases, but implants solve a different problem. They replace the missing tooth structure in a more complete way. That matters when you want stability, a more natural feel, and a replacement that supports daily life.

For patients comparing costs, it helps to think beyond the first invoice. A dental implant is a medical and restorative treatment, not just a product. When the plan is built carefully, you're paying for surgery, custom materials, precision, and follow-up care that supports the final outcome.

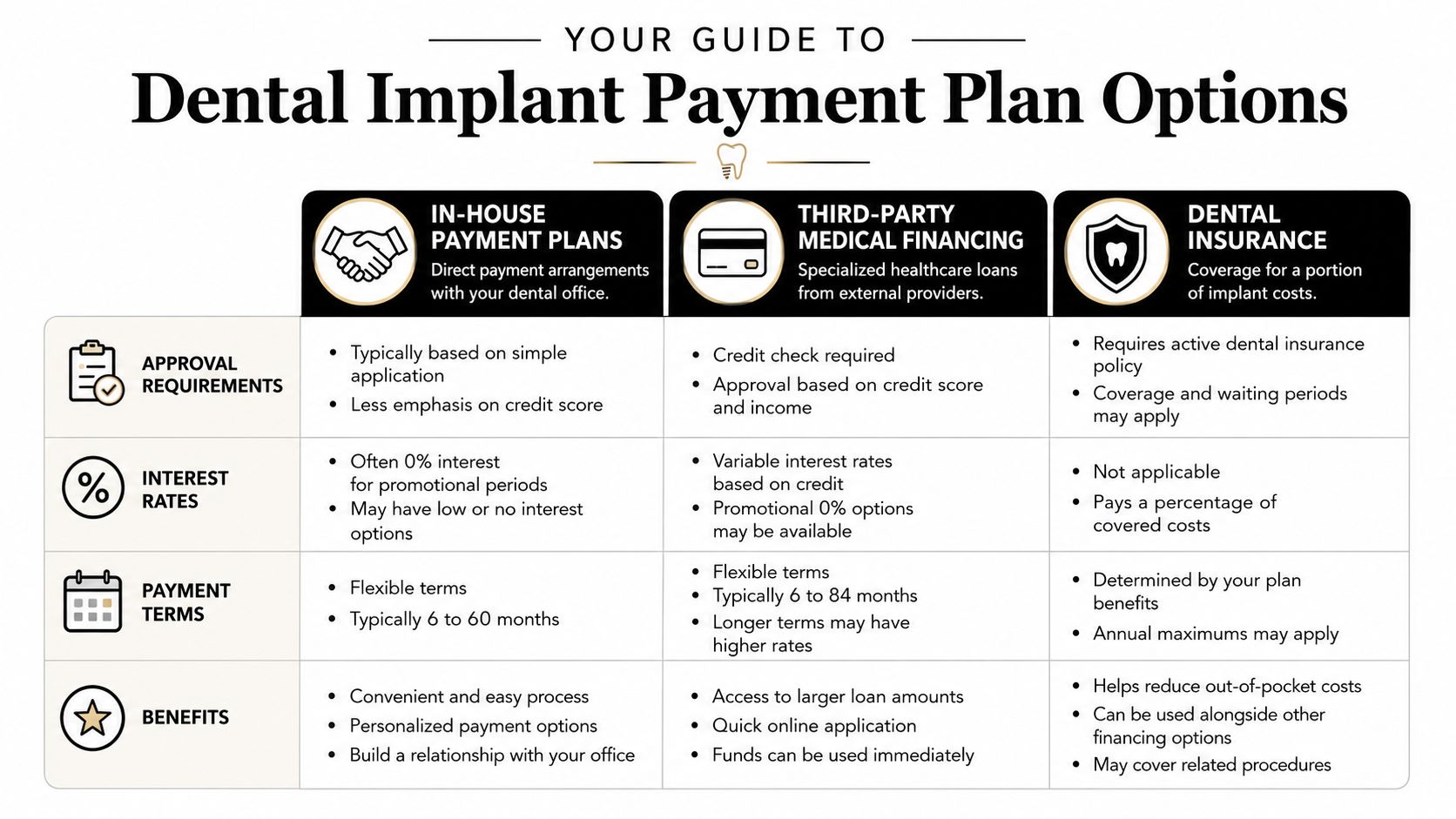

Your Guide to Dental Implant Payment Plan Options

A common patient scenario goes like this. You see one payment plan with a lower monthly number and feel relieved, then learn later that it stretches much longer or costs more overall. That is why the monthly payment is only one piece of the decision.

A better way to compare implant financing is to use the same approach you would use for a car loan or a mortgage. Look at the full amount you need to cover, how long you will be paying, whether interest applies, and what the total repayment could be by the end. Monthly affordability matters. Total cost matters too.

In-house payment plans

An in-house plan means the dental office lets you divide treatment fees into scheduled payments. The structure is often more direct than outside financing because you are working with the practice instead of a separate lender.

Many offices offer short-term installment arrangements, sometimes with a deposit and a defined payoff period. Terms vary by practice, so the important questions are simple. How much is due up front, how many payments will follow, and does the plan include interest or fees?

This option often fits patients who:

- Want a shorter repayment period

- Prefer simple terms they can review with the office

- May not want to open a separate credit account for a smaller balance

There is also an important detail patients often miss. “In-house” does not always mean “no credit check,” and “no credit check” does not always mean the same thing as a standard office payment arrangement. Some offices offer direct short-term splits based mostly on deposit and treatment timing. Others use a financing partner that advertises easier approval but still has its own rules, fees, or automatic payment requirements. Asking who is financing the treatment clears up a lot of confusion.

Third-party medical financing

Third-party financing comes from companies that focus on healthcare expenses. These plans usually offer longer repayment periods than office-based arrangements, which can make larger implant cases easier to fit into a monthly budget.

Smart Arches Dental notes in its guide to paying for dental implants that companies such as CareCredit, Proceed Finance, and Sunbit are common options for spreading treatment costs over longer terms. That can be helpful if your treatment is more involved or if a short payoff window would strain your budget.

This route may work well for patients who need:

- More time to repay

- A fixed monthly schedule for a larger balance

- A lender with formal approval terms and online application tools

A lot of patients also use pre-tax healthcare funds to reduce the amount they need to finance. If you are reviewing that part of the budget, this guide to HSA benefits for 2026 explains how these accounts can help with eligible medical and dental expenses.

If you want to see how a dental office may explain financing options in plain language, this payment plan information for dental work offers a helpful practice-level overview.

Before you choose any lender, ask for the details in writing.

Insurance and hybrid budgeting

Insurance usually lowers only part of implant-related treatment, so many patients build a layered plan instead of relying on one source. They may use insurance first, apply HSA or FSA funds where eligible, then finance the remaining balance.

That blended approach can make a big treatment feel more manageable because you are shrinking the amount that needs monthly financing. It also helps you compare offers more clearly.

Ask two direct questions before you sign. What will I repay in total, and what happens if I do not pay the balance off before a promotional period ends?

Those answers often matter more than the advertised monthly number. A plan that looks lighter each month can still cost more if the term is longer, if interest starts later, or if deferred interest applies after a missed deadline.

What Monthly Payments for Implants Could Look Like

A patient often feels the weight of treatment after hearing the words, “Your monthly payment would be about this much.” A full fee can feel distant. A number that has to fit beside groceries, rent, or a car payment feels immediate.

That is why monthly examples help. They turn a large treatment plan into something you can compare more clearly. They also reveal a mistake many patients make at first. The lowest monthly payment is not always the lowest-cost choice.

Example one with a single implant

Start with a single implant case. Earlier in this guide, we noted that single-tooth implant treatment can fall within a broad national price range. Once your insurance, deposit, or health account funds are applied, the remaining balance is what matters for financing.

If that remaining balance is financed over 12 months at 0% interest, the math is simple. A $3,000 balance is $250 per month. A $6,000 balance is $500 per month.

Longer terms usually lower the monthly number, but they can raise the total repaid if interest is added. That is a lot like choosing between paying off a small purchase quickly or stretching it out on a credit card. The shorter option can feel tighter each month, while the longer one can cost more by the end.

Example two with a full-arch case

Full-arch treatment changes the picture because the total fee is higher, and the gap between “manageable monthly payment” and “lowest total cost” gets wider.

If you are comparing a larger case, this All-on-4 implants cost guide helps explain what is usually included in a full-arch treatment estimate.

Here is the simplest way to read a full-arch payment offer. A 60-month plan may look far easier on paper than a 12-month plan. That can be true for your budget. It does not mean it is cheaper overall. The longer plan may be the right fit for one household and the wrong fit for another. The key is to compare both the monthly amount and the final repayment amount side by side.

Sample Dental Implant Monthly Payments

| Procedure (Total Cost) | 12-Month Plan (0% APR) | 24-Month Plan (Low APR) | 60-Month Plan (Standard APR) |

|---|---|---|---|

| Single Implant ($3,000) | $250/month | Lower than the 12-month payment | Lower than the 24-month payment |

| Single Implant ($6,000) | $500/month | Lower than the 12-month payment | Lower than the 24-month payment |

| Full Arch ($24,000) | $2,000/month | Lower than the 12-month payment | $400/month before any applicable financing costs |

| Full Arch ($50,000) | $4,166.67/month | Lower than the 12-month payment | About $833.33/month before any applicable financing costs |

Use this table as a starting frame, not a quote. Actual payments depend on the financed amount, the length of the plan, whether interest applies, and whether part of the treatment is paid upfront.

A payment that feels comfortable each month can still become the more expensive option if the term is longer or a promotional deadline is missed.

Patients in Chattanooga and Cleveland often tell us they feel calmer once they compare plans in one simple format: total treatment fee, amount financed, monthly payment, and total repaid. That side-by-side view is especially helpful when you are sorting through standard credit-based financing, office payment arrangements, and no-credit-check options, because those choices can look similar at first while working very differently in practice.

A printed estimate helps. So does taking the numbers one line at a time.

Applying for Financing and Improving Your Approval

Many financing applications feel stressful because patients wait until they're already in the chair to think about paperwork, income, or credit. Preparation changes that. If you know what lenders and offices are likely to review, you can gather what you need and avoid surprises.

The most important point is simple. Approval isn't only about whether you want implants. It's about whether the payment structure matches your financial profile.

What to gather before you apply

Bring the basics first. Most applications move more smoothly when you have:

- Photo ID and current contact information

- Proof of income, such as pay stubs or recent statements

- Insurance details if you plan to apply benefits first

- A treatment estimate so the financed amount is clear

Some patients also benefit from applying for a smaller amount after any insurance, HSA, or deposit has been accounted for. Financing less can make the approval path simpler.

The difference between credit-check and no-credit-check plans

Many individuals often get tripped up. Offices may advertise “flexible payment plans,” but those plans don't all work the same way.

Most content fails to explain the critical difference between in-house payment plans with active credit checks versus 'no-credit-check' in-house plans that rely on income verification and upfront deposits, a nuance missing from 2025–2026 financing guides, as noted in this discussion of implant financing options in Texas.

A standard in-house or third-party plan may review your credit profile as part of approval. A no-credit-check option may focus more on documented income, a stronger initial deposit, and a shorter repayment timeline. That can help some patients who have bruised credit but stable income. It can also mean less flexibility in how long you have to pay.

Practical ways to improve your odds

Not every patient needs to do all of these, but these steps often help:

- Check your credit before applying. You don't need perfect credit, but you should know what lenders may see.

- Reduce the amount requested. Insurance, HSA funds, or a deposit can lower the financed balance.

- Complete forms carefully. Small errors can slow down or derail approval.

- Ask whether a co-signer is allowed if that's an option in your situation.

- Compare the actual terms. Some approvals look good until you read the repayment details.

Some patients are denied on the first option and approved on the second. A “no” from one lender doesn't always mean treatment is off the table.

Patients who need dental implants near me often assume financing is one yes-or-no gate. In reality, it's a set of options. If one path doesn't fit, another one may.

Financing Your New Smile at Winn Smiles

A good financing conversation should feel as clear as a treatment conversation. You should know what care is recommended, what it costs, what your options are, and which payment path fits your life without creating extra strain.

That's especially important for larger treatment plans like implants, full-arch restoration, or cases that also involve tooth extraction, dental x-rays, and follow-up restorative work. The right payment structure should support treatment, not compete with your ability to handle everyday expenses.

A practical affordability benchmark

One of the most helpful guidelines for patients is this. Financial experts and industry guidelines recommend that dental implant payment plans should not exceed 10% to 15% of a patient's monthly discretionary income to prevent undue financial strain and ensure long-term stability, according to this overview of how to finance dental implants.

That benchmark matters because it shifts the discussion away from “Can I get approved?” and toward “Will this feel manageable over time?” Those are not the same question.

What a patient-centered visit should feel like

For many people looking for a dentist near me in Chattanooga or Cleveland, the financial side is tied directly to trust. A strong visit should include:

- A clear exam and diagnosis so you understand whether implants, same-day crowns, or another restorative option makes sense

- Straightforward cost discussion with enough detail to compare plans

- Support with next steps if you're using insurance, pre-tax healthcare funds, or outside financing

- A comfortable pace so you can make decisions without pressure

Patients often come in asking about one issue and discover they also need routine cleaning and exams, a new patient exam, or cosmetic updates such as teeth whitening later on. A helpful office keeps those priorities organized instead of stacking everything into one confusing recommendation.

Winn Smiles offers implant treatment along with payment plan options and financing support for dental work, so patients can compare approaches based on treatment needs and budget fit rather than guessing from ads alone.

Your Questions About Implant Payment Plans Answered

Can dental insurance help with implants

Sometimes. Insurance often helps with parts of treatment, such as an exam, imaging, extraction, or restoration, but it usually does not cover the full implant process. For many patients, insurance lowers the amount that needs to be financed rather than replacing financing altogether.

Are implants worth financing for the long term

They can be, especially if you are comparing total value instead of focusing only on the monthly payment. A lower monthly amount can feel easier at first, but the better question is how long the restoration is expected to serve you and what the full financing cost looks like over time.

Dental implants have a strong long-term track record. Dental implants demonstrate exceptional long-term durability with a cumulative survival rate exceeding 90% over 10 years and remaining functional for approximately 86% to 92% of cases after 20 years, according to this review of implant success rates, costs, and growth trends. That long service life is one reason many patients see financing as a way to spread out the cost of a treatment designed to last.

What if I'm denied financing

A denial can feel discouraging, but it usually does not close every door.

Some patients qualify with a different lender. Others do better with an in-house plan, and that is where the details matter. A no-credit-check option and a standard in-house plan are not always the same thing. One may require different down payment terms, shorter repayment windows, or tighter treatment limits. Asking about those practical differences can save a lot of confusion, especially for patients in Chattanooga and Cleveland who are trying to find a workable path with past credit challenges.

Another option is to phase treatment. That can reduce the amount you need to finance at one time.

What should I ask before agreeing to a payment plan

Ask for the full treatment fee in writing. Then ask what the plan adds to that number.

Helpful questions include whether interest applies, whether there is a deposit, how long the repayment term lasts, whether there are missed-payment fees, and what happens if a promotional balance is not paid on time. It also helps to ask one simple question that many people skip: “What will I pay in total by the end of this plan?” That question turns the conversation from “Can I fit this monthly payment into my budget?” to “Is this the best financial choice for me?”

For those seeking a dentist in Chattanooga, TN, dentist in Cleveland, TN, or a cosmetic dentist near me, the clearest next step is a personalized consultation. A real exam and written estimate give you something much more useful than an online price range. You can see your treatment needs, compare payment options side by side, and choose based on total cost and monthly comfort, not guesswork alone.

If you're ready to talk through implant options, costs, and monthly payment choices in a calm, practical way, contact Winn Smiles. A consultation can help you understand your treatment needs, compare financing paths, and decide on a plan that supports both your smile and your budget.